Ohio's 2023 Rental Market — The Good, the Bad, and the Ugly

A Brief Summary of Ohio's 2023 Rental Performance

As we near the end of 2023, it’s time to briefly recap Ohio’s fluctuating rental market and discuss some aspects of 2024’s forecast.

Affordability and Accessibility

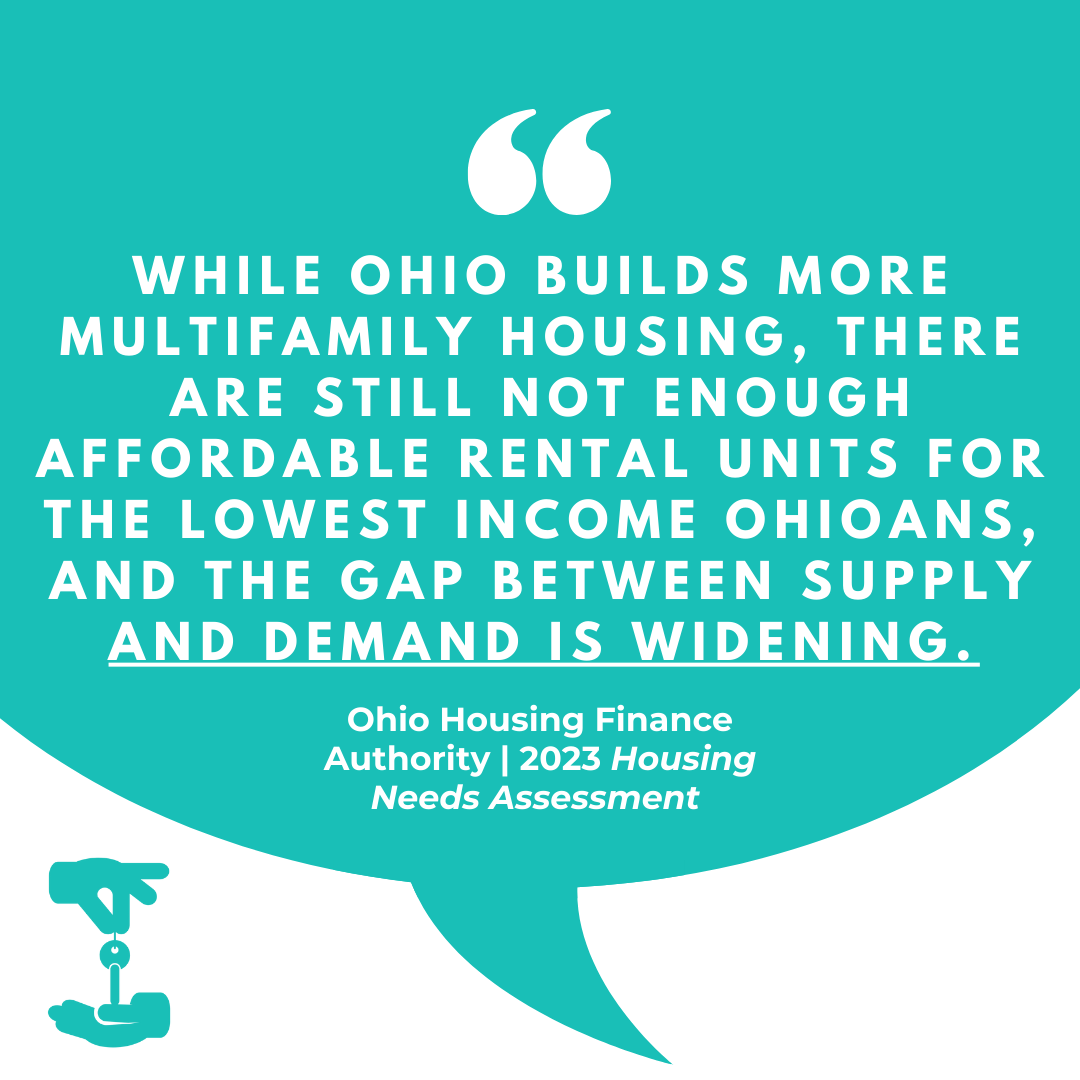

The Ohio Housing Finance Authority’s annual Housing Needs Assessment gave us great insight into some aspects of Ohio’s unpredictable rental market. We saw the lowest recorded rental vacancy rates in 2021 (4.0%), and then 6.2% at the end of 2022. The rate reported as of the end of 2023Q2 varies slightly depending on the source, but we’ve seen a consensus that hovers around 5.1%. It’s no secret that finding affordable rentals is difficult, but the lack of available units may be attributed to the extreme buy-ups of properties for “seasonal, recreational, or occasional use” (think of Airbnbs and the like.)

When you pair the lack of available units with the rising rent costs and a stagnant income level, the outcome will never be positive. Keep in mind that, at the time of writing this, Ohio does not currently have any rent caps or rent-control laws. The OHFA reports that over 700,000 people in the state’s rental households are severely cost-burdened, which means that half or more of their monthly income is spent on their rent. Average monthly rents in Ohio this year (again, vary across sources):

Cleveland and Akron markets saw some of the highest rents in Ohio this year; however, average incomes could not match the increase in rental costs. A

report from the Low Income Housing Coalition revealed that the average renter brings home about $18.47 an hour (reminder: Ohio minimum wage is still $10.10) and with one in three Ohioans renting rather than owning, common job wages are not keeping up with the rent increase. In Columbus, rents have jumped 5% higher after inflation than the national average, and Franklin County incomes are lower than the country’s average.

Multi-Family Units

RealPage’s industry research has suggested that the decrease in construction of multifamily starts is more than likely 3-4x higher than the U.S. Census Bureau’s previous estimate of 12%--this could be attributed to a plethora of issues, as revealed by RealPage:

1. The American Institute of Architects documented “15 consecutive months of declined billings for multifamily,” signaling a steep drop in interest in residential apartment construction from multifamily-specific businesses

2. Delays in development—a collective lack of construction financing

3. In tandem with #2, a substantial amount of bank lenders have added more restrictions to lending standards for construction in 2023 (Nearly 3/4 of U.S. banks!)

4. So, what happens when these roadblocks perturb equity investors’ ability to build assets? RealPage suggests that they are choosing to buy cheaper, existing assets instead of waiting around on ground-up development.

The multifamily market saw a shift from supply to demand this year and throughout 2024 and can expect vice versa in 2025-2026. More multifamily construction projects are being completed than kick-started this year, and we can expect to see deliveries top off through 2024. Starts are not projected to expedite in a considerable way, so RealPage warns that we will probably see lower supply through the next few years.

While this is a national analysis, it heavily applies to Ohio’s multifamily market. Multifamily News’ most recent report of Columbus’s market, via metrics from Yardi Matrix, showed a .2% growth in demand for multifamily units during a three month period.

Cincinnati, on the other hand, saw itself rise to the top of the nation’s rental ratings in 2023. Multiple articles from sources such as Yardi and RealPage have reported on the Queen City’s exceptional numbers, including its rankings as the 43rd largest multifamily market (116,828 completed units; 25,827 in development) and 36th in year-over-year rent growth, and is projected to maintain its presence as a top rental market into 2024. However, only time will tell! Be sure to check our website and social media platforms for updates and insights into this ever-changing industry.